1168

Views & Citations168

Likes & Shares

The African Continental Free Trade Agreement (Afcfta) is seen as one of the possible responses for the continent to the COVID-19 crisis’ economic impact. Building long term continental resilience and improving volatility management, through accelerated export diversification could be achieved through a rapid and ambitious implementation of the AfCFTA. This paper analyzes the impacts of the external demand dimension of the Covid-19 crisis in a context where African countries are preparing to make the continental free trade area effective in January 2021. Against a unique Covid-19 time that will strongly transform production and trade processes across the world, the paper explores to what extend a rapid implementation of the AfCFTA, supported by Trade Facilitation reforms could play a key role in mitigating the severe economic consequences of Covid-19. Our results indicate that maintaining the momentum towards an ambitious AfCFTA’s implementation is crucial as several African countries will face a strong negative economic impact. Indeed, a successfully implemented AfCFTA will empower the region to more successfully navigate the hit the region’s economies are facing. In the case of an immediate implementation for all African countries the drop in Africa’s GDP would be significantly mitigated. The decreasing world demand is then partially compensated by new export possibilities across the continent for African economies, due to the removal of intra-African trade tariffs. African countries might consider supporting immediate trade facilitation measures, and more fundamentally address facilitation along the entire length of corridors across the continent. These moves would counter-balance the rising trade costs, improve the capacity of African countries to better benefit from the re-organization of global value chains, and strengthen regional value chains - thus mitigating economic and social impact of the crisis, through new business opportunities.

INTRODUCTION

Beyond the direct dramatic human consequences, the COVID-19 crisis will have a long-term, strong adverse impact on Africa as it severally hits its economies. The more recent evaluations[1] (IMF, 2020) estimate for 2020 a contraction of the GDP for the main economies of the continent, compared to 2019 (Algeria -5.5 percentage points, Morocco -7.0, Nigeria -4.3, South Africa -8.0). Indeed, given the oil and commodities shocks[2], decreases in labor productivity and total factor productivity, and increased costs of international trade that will particularly hurt smaller economies, Africa is particularly exposed. Moreover, the virus will impact sustained development goals (SDGs) and poverty alleviation while African exports should decrease by -13,5% (-23,5% for agro-food and -15% for industry) with the current trend (IFPRI, 2020).

Pro-active, large-scale and integrated measures across all policy areas are necessary to make strong and sustained impacts. Several immediate responses are then required, notably with immediate health response through procurement of surveillance and logistical supplies and involve all stakeholders. Socio-economic impacts should be mitigated through fiscal stimulus and accommodative monetary policies (ECA 2020) coupled with liquidity management in the financial sector.

Given the importance of the informal sector in Africa and the insufficient social protection into the formal one, a particular effort is urgently needed to increase funding for social protection (ILO 2020), through existing schemes and/or ad-hoc payments for workers, including informal, seasonal and migrant workers, and the self-employed.

In addition to these measures, it is crucial to support and involve the economic operators and particularly the private sector in the response to the crisis. Covid-19 is at the same time a supply shock and a demand shock, and both aspects will impact international trade in goods and services (Baldwin and Tomiura, 2020; WTO, 2020).

Trade in manufacturing sectors will be particularly affected given the global disruption of the supply chains in the main global trading countries (WTO, 2020: ECA, 2020). African economic operators will be affected by a deep reorganization of global value chains (GVCs). The Covid-19 crisis revealed that GVCs concentrated in a single region may not represent an optimal investment in terms of security (for governments), as well as in terms of risk (for companies). A strong dynamic of GVC diversification, with an important regional component, will emerge. In this context, the AfCFTA will be a strong lever for building regional value chains (RVCs) in Africa and contribute to both export diversification and export sophistication. The AfCFTA has the specificity that it will impact positively mainly manufacturing trade (see Mevel, Moll de Alba and Oulmane, 2016). Beyond trade Covid-19 is also affecting all types of foreign investment. UNCTAD data suggest downward pressure on FDI will be -30% to -40% in 2020-2021.[3]

At the continental level, it is then important to assess if maintaining the momentum towards AfCFTA’s implementation and trade liberalization schemes could represent a real trade lever for African countries facing a strong negative impact on their trade with the rest of the world (WTO, 2020). One could think that African economies could show additional ambitions in attracting and retaining investment first to maintain their firms’ linkages with MNEs in the global production networks and supply chains, but also to promote new investment related to foster new regional value chains within the AfCFTA framework. Against this context, many observers call for an ambitious implementation of the AfCFTA and also to resist the temptation to protectionist measures (UNSG report, 2020). The objective of the paper is precisely to assess this scenario and capture the potential of this agreement. Obviously, full implementation will take time, adjustments costs required, and the process will not derive full gains in a very short period of time. Taken into consideration this caveat, our simulation seeks to provide empirical evidences about the expected gains of the AfCFTA full implementation.

In a context where African countries are preparing to make the continental free trade area effective, against a unique and disruptive Covid-19 time that will strongly transform production and trade processes, to what extend a rapid implementation of the AfCFTA, supported by trade facilitation reforms such as the WTO Trade facilitation Agreement (TFA) could play a key role in mitigating the severe economic consequences of Covid-19? This study contributes to bring quantitative elements that will further document the debate on the necessary framework, reforms and investments for a pooled African market that will help African countries to transform the Covid-19 crisis into an opportunity to harnessing the full potential of the AfCFTA in support of SDGs and agenda 2063 realization. To do this, we used a global computable general equilibrium model to simulate consequences of external demand Covid-19 shocks, in combination with the African continental free trade agreement scenarios and trade facilitation reforms.

The article first describes the world CGE model, data and the scenarios simulated. The third section presents and discusses the results. In the fourth section, we highlight the limitations of our study and their implications on the results. Finally, the section 5 concludes and gives policy recommendations.

THE CGE MODEL, DATA AND SIMULATIONS

General Description

The CGE model used in this study is based on the multi-region dynamic model developed by Lemelin et al. (2013). The firms operate in a perfectly competitive environment by maximizing profits/minimizing costs given their production technology constraint and the prices of goods, services and factors (price-taking behavior). There are two regional agents. The first agent is the government that collects taxes and pays for public expenditures. The second agent is households who receive the rest of the regional agent’s income (labor and capital income) and pay for private expenditures. Tax instruments include income taxes, taxes on goods and services and on imports, and taxes on production. For imported goods and services, taxes are applied on the sales value that already includes trade and transport margins, and customs duties. Domestic demand for commodities, whether imported or produced domestically, consists of household demand, investment, public administrations demand, and intermediate consumption. Producers are assumed to allocate output to market outlets so as to maximize sales revenue. Nested CET functions govern producer’s behavior. On the upper level, aggregate output is allocated among three market outlets: exports, domestic and international transport margins. On the lower level, the exports are distributed between regions of destination. The behavior of the Buyer is symmetrical to producer behavior, as it is assumed that local products are imperfect substitutes for imports, and imports from one region are an imperfect substitute for imports from another region (heterogeneous goods hypothesis represented by CES aggregator functions).

Macroeconomic Equilibriums, Closures and the Dynamics

As far as macroeconomic equilibriums are concerned, in commodities and factor market, supply and demand equilibrium are assumed to be verified thanks to flexible respective prices. In the baseline scenario, labor demand is assumed to be equal to labor supply (full employment) in each region. The model includes 5 African regions (North Africa, West Africa, Central Africa, Eastern Africa, South African countries) and 11 non-African regions (Oceania, East Asia, South Eastern Asia, South Asia, Latin America, European Union, Rest of MENA, USA, Canada, Rest of North America, and the Rest of the world)

As far as closure rules are concerned, the numeraire is the exchange rate of a region chosen as the reference region: European region, while regional GDP deflators are fixed. Public savings are fixed and real public expenditures are flexible.

The dynamics of the model is a recursive one. The calibration of the baseline scenario is performed by running a modified version of the model which is constrained to follow Fouré et al. (2012) real GDP projections and where the total factor productivity (TFP) is endogenous. Labor supply and aggregate domestic saving rates are also set according to Fouré et al. (2012) projections. The solution value of the total factor productivity and other exogenous variables (including savings rates) given by the modified version of the model constitute the baseline scenario. These variables are then set exogenously fixed at their calibrated values in the model.

Capital accumulation does not follow Fouré et al. (2012) projections but is endogenous in the model. So, the stock of sectoral and regional capital is equal to the stock of the preceding period, minus depreciation, plus the volume of new capital investment in the preceding period.

The quantity demanded of each type capital in each region is equal to the quantity supplied. Capital is assumed to be region and sector specific. Total investment expenditure equals the sum of agents’ savings – including households and government – plus the amount of depreciation.

It is assumed that the labor is mobile only between the production sectors of the same region. Thus, labor can move between the sectors but not from one region to another. So, the wage rate is assumed to be defined by region within a geographically segmented labor market.

Data & Simulations

The data used to carry out the simulations are the most recent data from the Global Trade Analysis Project (GTAP10.2) that cover 57 sectors and 141 countries/regions. The sectors have been aggregated into 18 sectors, and the countries/regions into 16 regions including the 5 African regions[4] listed above.

Recognizing that COVID-19 is much more than a demand shock on the global GDP, a full assessment of the impact on the African economies should explore the different impact channels. However, as this article aim to explore different levels of an identified policy response to a decline in external demand, the scenarios will mainly concentrate on this dimension. We simulate then 2 scenarios to assess the impact of the decline in external demand related to the Covid-19 crisis on African economies:

The first theoretical scenario (COVID1) incorporates a World GDP level at -4%. This scenario reflects a 1-point worse scenario of disturbance of the crisis on the economic sphere compared to the last April IMF’s WEO forecasts a -3 % world GDP in 2020.

The second scenario (COVID2) is based on a deepening of the Covid-19 crisis with the continuation of strong social distancing policies that are disturbing the main economies and resulting to a -8% world GDP growth. As the previous one, this scenario does not include mitigation measures.

These two scenarios will illustrate to what extent African countries could be impacted by the crisis without mitigation measures such as stimulus packages and/or strong coordinated policies at the continental level, particularly ones related to the deepening of regional integration through the AfCFTA.

The remaining scenarios explore policy responses based on the pooled African market using the AfCFTA as strategic levers to transform the Covid-19 crisis into an opportunity to develop RVCs and achieve the continental integration.

The third scenario (AfCFTA) is based on the first scenario (World GDP at -4%) in addition to the implementation of a AfCFTA through the immediate dismantlement of 90% intra-African tariffs, in accordance with the agreement’s modalities[5].

The fourth one (AfCFTA TF) is based on the third scenario (-4% and AfCFTA), and with a trade facilitation policy implemented at the continental level, that will reduce trading costs by 10% (see Mevel, Moll de Alba and Oulmane 2016, or Zidouemba and Sadni Jallab, forthcoming).

The fifth scenario (AfCFTA HC) is a variant of the third scenario (-4%, AfCFTA), with, in addition, an increase in trading costs due to trade restrictions measures across the world and the disruptive impact on logistics and transport. Based on the literature and recent estimates from the WTO (2020), we assume a 5% global increase on trade costs[6]. This 5% increase is derivated from a very detailed empirical investigation done by the WTO (2020), where they aggregated all indirect costs due the Covid-19. The computation of the trade weighted average percentage increase in ad valorem trade costs for the world represents an increase of 3.4%. Given that many regions had to face a second wage of the Covid-19 with similar and additional economic effects, we suppose that it has impacted the trading cost and we consider as a proxy a 5% increase at the global level.

Finally, the last scenario (AfCFTA HCTF) is equivalent to the 5th scenario, with a trade facilitation policy implemented at the continental level. WTO (2015) estimated that a full trade facilitation agreement could represent an equivalent of about 14,5% trade cost reduction. We consider in our simulation that trade facilitations measures will reduce trading costs by 10%, as simulated in the fourth scenario.

RESULTS AND DISCUSSION

The impact of Covid-19 on African economies: A strong macroeconomic recession

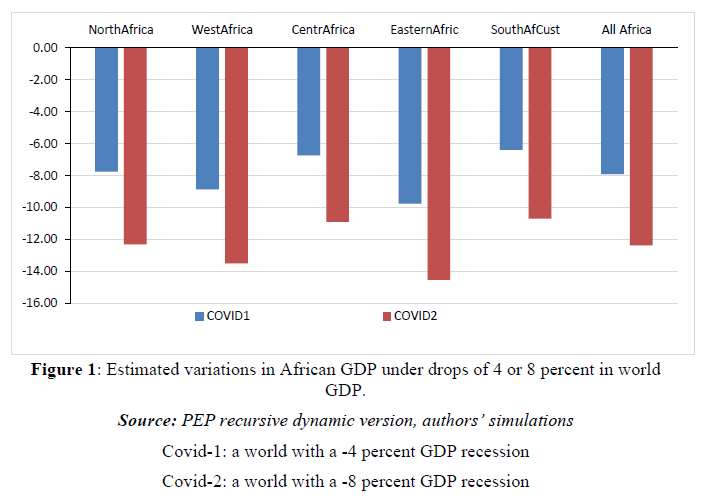

The figures below summarize the macroeconomic and sectoral impacts for Africa of the two first scenarios, world recession with GDP at -4% (COVID1) and -8% (COVID2).

Overall, in the first scenario, we find that the continent will experience a decrease of 7.76 percentage points in GDP (Figure 1). In a second scenario, we estimate that loss to be 12.31 percentage points. Notably, we estimate that Eastern and Western Africa will be hardest hit, respectively, with decreases in GDP of -9.76 and -8.87 percentage points, respectively, in the first case and -14.55 and -13.51 percentage points in the second case.

These two sub-regions are the ones experiencing the stronger trade shock in term of decrease in their exports. Beyond minerals, gas and oil exports, electronics equipment’s production and exports are particularly affected in these two regions leading to significant job losses as illustrated by ILO (2020).

These results are coherent with the IMF April forecasts that consider that the Covid-19 will lead to a -3% global recession, and in the case of Sub-Saharan Africa, a variation of 4.7 percentage points (-1.6 instead of 3.1 in 2019) including the stimulus packages to mitigate the Covid-19 shock. From it side, the World Bank estimates (on April 9) a contraction of Sub-Saharan African GDP in 2020 of between 2.1 and 5.1% (the second scenario being the most likely). This represents 7.5 points less than expected.

In term of income losses if the magnitude is similar, the situation is different from a sub-region to another. If Eastern and Western part of Africa experience the highest losses for public income as it is the case for GDP, it is the southern part of the continent that experiences the highest losses in term of household’s income. East and West Africa that experience the highest households’ losses. The structures of the economies in term of sectoral contribution to the income is one of the explanations of these differences. Two main messages could be drawn from this: i) the measures should be differentiated and tailored to the specificity of each region and country; ii) The decline in household and public income will strongly affect public accounts and increase public deficit leading to debt management challenges Figure 2.

The AfCFTA, a lever to mitigate the Covid-19 crisis and an opportunity to build regional value-chains

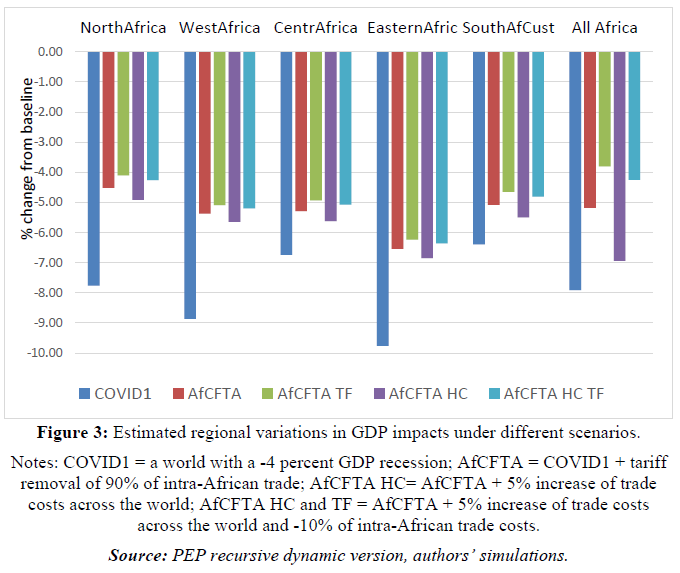

Beyond the debate on the moratorium or cancellation of the debt to create a policy space to mitigate the Covid-19 crisis, African countries should also explore how to leverage from internal means, involving economic operators and the private sector. Our evaluation of the impact of a full implementation of the AfCFTA according to the modalities indicate that in the case of a -4% world GDP, the negative change of the GDP in Africa is -5.2 instead of -7.9 percentage points if 90% of intra-African tariffs are removed according to the AfCFTA modalities. The mitigation represents a gain of 2.7% of the African GDP (AfCFTA scenario in Figure 3). At the sub-regional level, this mitigation effect is particularly important for Eastern Africa (3.5% of the GDP) and North and West Africa (3.2%). The mitigation effect could be magnified if the implementation of the AfCFTA is coupled with trade facilitation (TF) measures that would reduce trade costs by 10%. The change in the GDP would be in this case -3.80 pp, bringing the mitigation to a gain of 4.1%.

To take into consideration the disruptive effect of the Covid-19 on the value chains and more particularly on trade operations, but also on expected trade restrictions measures, we stipulate that trade costs could experience an increase in the short term. We approach this element in the AfCFTA HC through a 5% additional trade cost for all countries across the world. In that case the implementation of the AfCFTA will reduce the Covid-19 impact from -7.9 to -6.9 percentage points of GDP, bringing the AfCFTA mitigation’s potential from 2.5 point of GDP to only 1-point.

It is then crucial for African countries to support trade immediate trade facilitation (TF) measures to counter-balance the rising trade costs, but also to improve the capacity of African countries to better beneficiate from the re-organization of GVCs and redeployment of activities in particular, but also to encourage the development a regional value chain.

This AfCFTA HC and TF scenario include a reduction of 10% of trade costs among African countries, while the 5% increase is still present all over the world. The impact on the mitigation’s potential of the AfCFTA is significant, as the change induced by the Covid-19 is reduced from -7.9 to -4.3, increasing the potential to 3.6 point of GDP Figure 4.

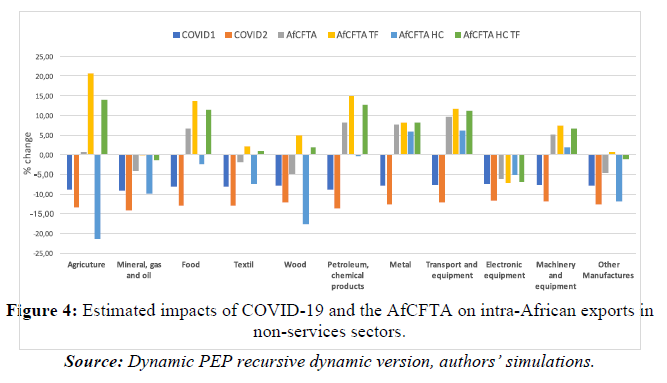

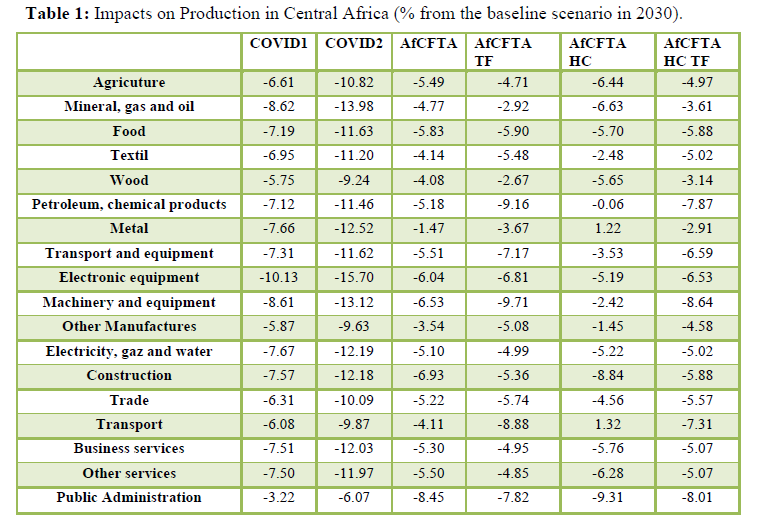

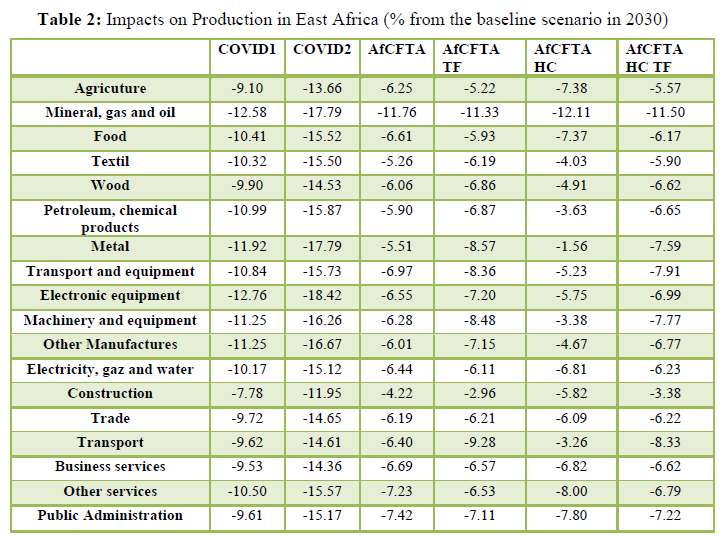

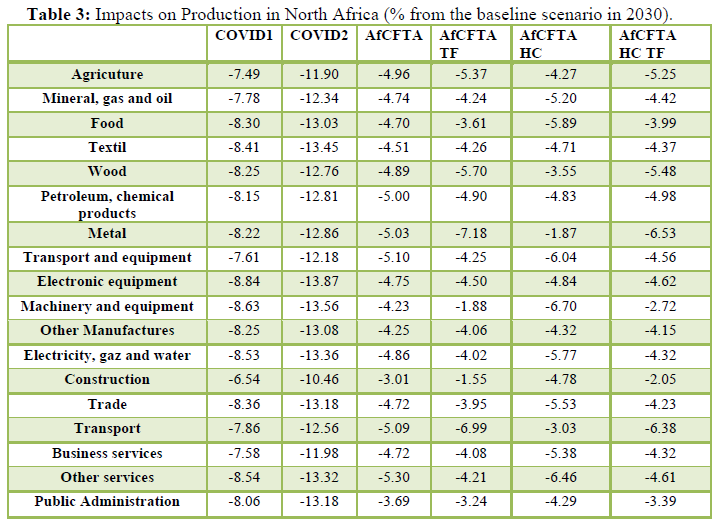

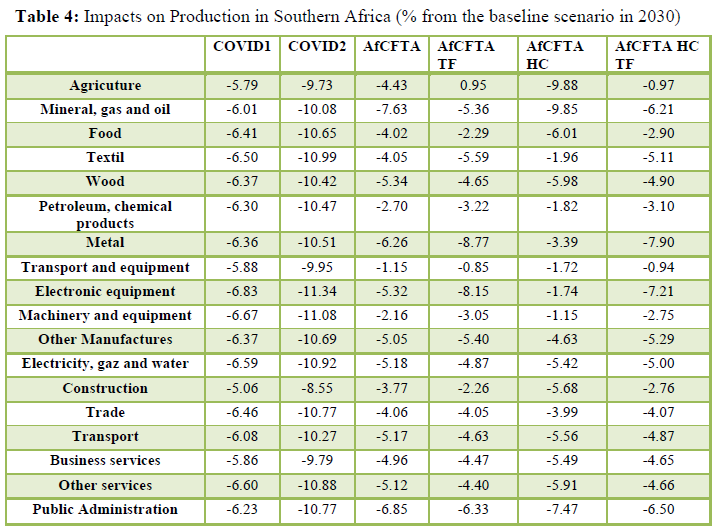

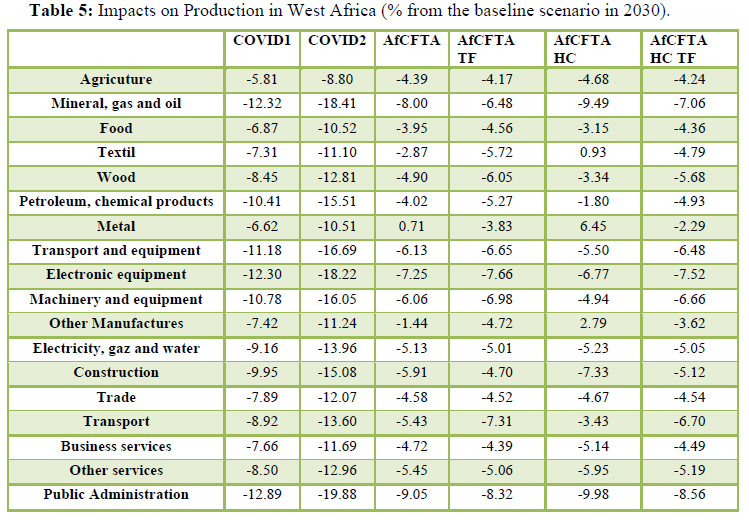

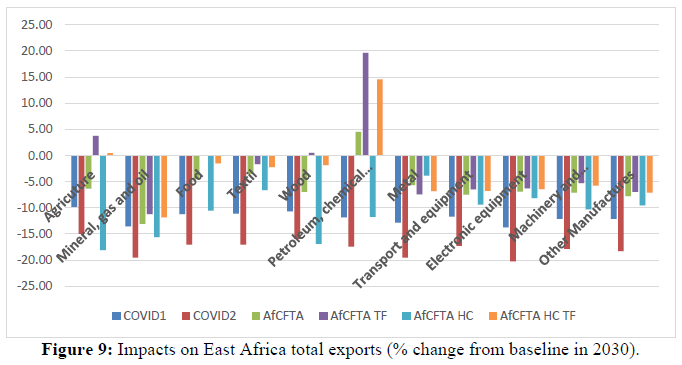

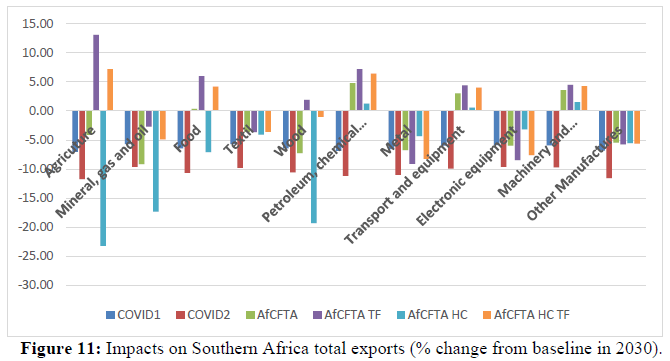

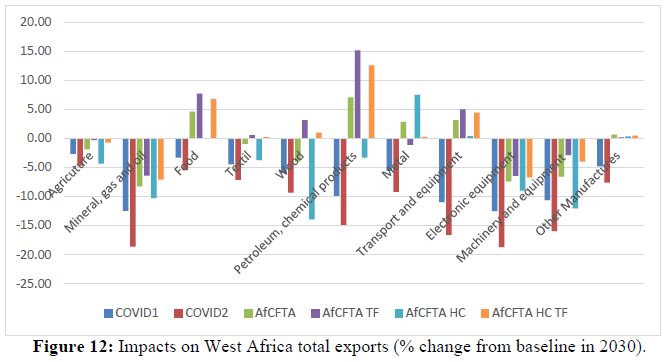

The global recession leads to a drop in the purchasing power of foreign consumers, and therefore a decrease in African exports (Figures 4 & 5), at the origin of the drop in sectoral production. Indeed, the sectoral productions decrease by a range of -5% to -13.1% depending on regions and sectors (see Tables 1 to 5 in appendices). Whereas in the AfCFTA scenario, the decrease in production is significantly mitigated, African trade facilitation reforms play, as expected, an even more important role in mitigating production decline.

Exports between African regions are being boosted by the AfCFTA, particularly when accompanied by trade facilitation (TF) reforms allowing African countries/regions to better take advantage of the incentives offered by the AfCFTA (Figure 4). At the sectoral level, TF reforms have a strong impact on agriculture, food, and petroleum and chemicals. All these sectors play a crucial role in food security of African populations. TF reforms could thus make it possible to achieve appreciable results in terms of food security.

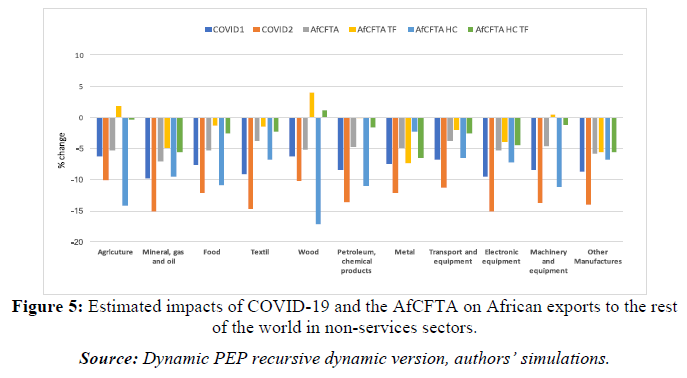

Figure 5 illustrate that the AfCFTA scenarios (the four last scenarios) is not the cause of a net trade diversion at the sectoral level from extra to intra African exports. Indeed, the reduction of exports toward the rest of the world (COVID 1 and 2 scenarios) are not amplified by the implementation of the AfCFTA. It is only when we consider an increase of trade costs (AfCFTA HC) that we observe a further reduction of African exports towards the rest of the world.

By focusing more on the total exports of each African region (Figures 5-9), we can still see that the growth of trade obtained in the AfCFTA scenario is amplified with TF reforms. Similarly, the export structure obtained in the AfCFTA scenario is maintained under the TF measures scenario. It is also very important to emphasize the diversification of production and exports in the AfCFTA scenario since the strong growth of the production (or exports) of a given sector is not done at the expense of another.

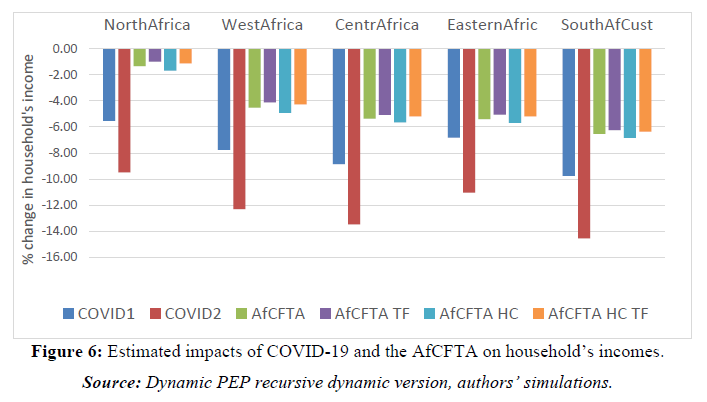

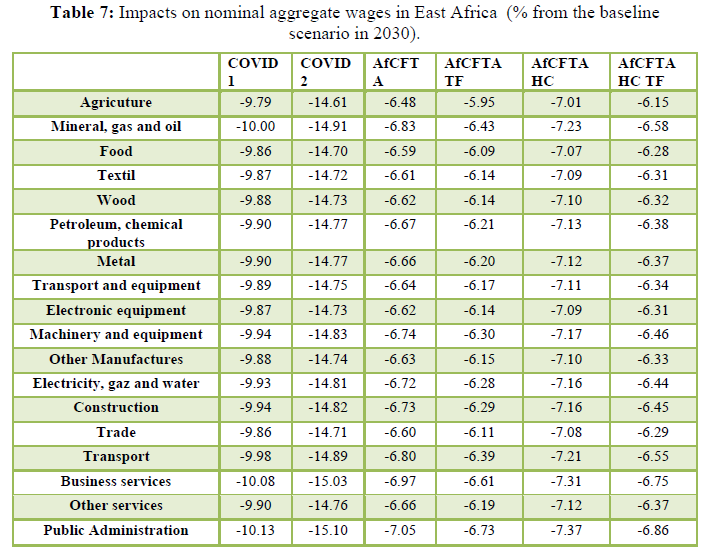

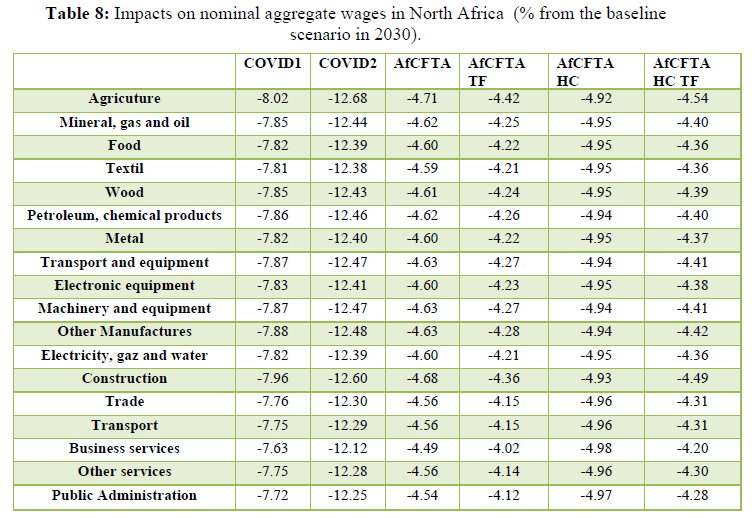

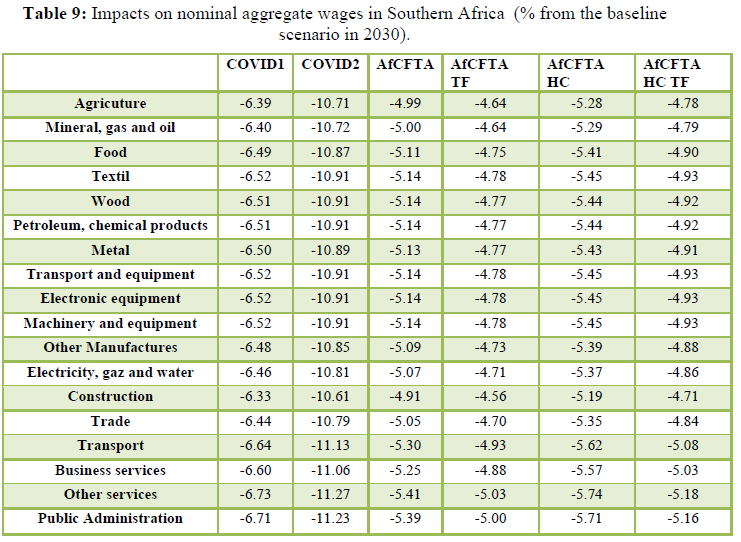

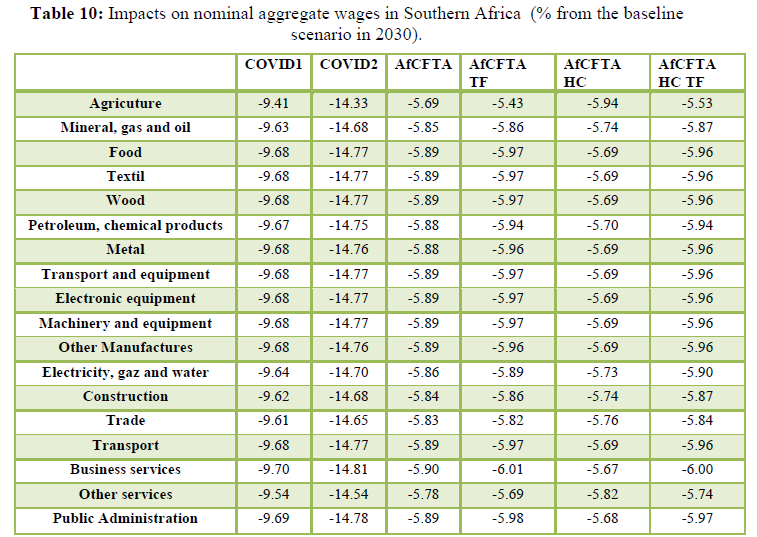

Figure 6 shows the magnitude of the AfCFTA mitigation effect on household’s income in the different African regions. As we have seen before (Figure 2), the COVID1 and COVID2 scenarios have a strong negative impact on the different regions (from -5.5% for North Africa to -9.8% for Southern Africa in the case of COVID1). The implementation of the AfCFTA would significantly reduce this negative shock on the household’s income. In North Africa the AfCFTA HC TF scenario will reduce this impact to -1.1%, while in Southern Africa, it will bring it to -6.3%, leading to a substantial mitigation of the reduction in living standards of the representative households following the COVID-19 crisis.

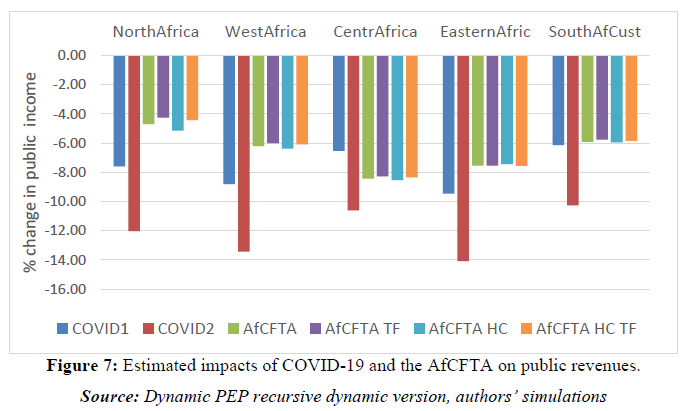

The decrease in customs revenue due to tariff cuts under the AfCFTA causes a decline in the public revenues for most African regions. However, by allowing production and exports to increase and household income growth, leads to a more than proportional increase in domestic tax revenues (in particular taxes on incomes and value added taxes). This results in a substantial reduction of the public revenues losses related to the COVID-19 impact (Figure 7).

These macroeconomic results are in line with some previous studies on the effects of removing barriers to intra-African trade (see for example Zidouemba and Sadni Jallab 2020). The AfCFTA has a significant positive impact on growth and income and represents a real policy lever to mitigate the negative economic impact of the COVID-19, particularly on trade and production. Moreover, we argue that specific trade facilitation measures that target identified weaknesses and bottlenecks that hamper the development of regional value chains. If organized through an appropriate institutional framework, far from being a threat to the African economies, ambitious trade facilitation reforms may represent an opportunity for trade creation and diversification, as well as for African economies industrialization.

RESEARCH LIMITATIONS AND METHODOLOGIC CAVEATS

The results presented above should be interpreted with the awareness of some limitations. We can identify two major technical limitations. First, the modeling does not take into account unemployment and/or underemployment, which are widespread in African countries. Failure to take into account unemployment can have specific implications on the results. Indeed, we can imagine that labor mobility, in the presence of unemployment would induce, in a first step, a decline in unemployment without effect on real wage rates, the adjustment by wage rates taking place, in a second step, only when there is a total absorption of unemployed workers. In this context, the availability of an unused stock of labor implies that the increase in expected sectoral productions, exports, real incomes and real GDPs may be greater than what has been achieved in this paper. Our results may therefore have been underestimated in the absence of taking into account unemployment. Therefore, this does not change the orientation of our results.

The second limitation concerns the level of aggregations of African regions. Indeed, this aggregation, while it has the advantage of facilitating the resolution of the model, can hide disparities between several countries belonging to the same region. Nevertheless, although we cannot control the heterogenous effects among African countries, our results allow capturing a global assessment at the continental level and as the AfCFTA is design at the African level, this analysis offers interesting perspectives.

CONCLUSION AND POLICY RECOMMENDATIONS

In this paper, we have been interested in the impacts of the Covid-19 crisis in a context where African countries are preparing to make the continental free trade area effective in January 2021. Against a unique Covid-19 time that will strongly transform production and trade processes across the world, we explored to what extend a full implementation of the AfCFTA, supported by Trade Facilitation reforms could play a key role in mitigating the severe economic consequences of Covid-19. Indeed, beyond the immediate sanitary, social and economic responses, it is crucial to support and involve the economic operators and particularly the private sector in the long-term response to the crisis. Our results indicate that maintaining the momentum towards an ambitious AfCFTA’s implementation is crucial as several African countries will face a strong negative economic impact. Indeed, a successfully implemented AfCFTA will empower the region to more successfully navigate the hit the region’s economies will take (and are already taking). In the case of an immediate implementation for all African countries, the drop in Africa’s GDP would be significantly mitigated. The decreasing world demand is then partially compensated by new export possibilities across the continent for African economies, due to the removal of intra-African trade tariffs.

In addition to the AfCFTA, African countries might consider supporting immediate trade facilitation measures, and more fundamentally address facilitation along the entire length of corridors across the continent. These moves would counter-balance the rising trade costs, improve the capacity of African countries to better benefit from the re-organization of GVCs, and strengthen RVCs-thus mitigating economic and social impact of the crisis, through new business opportunities, counterbalancing the deflating pressures on production and salaries. With these potential impacts in mind, as Africa faces Covid-19 head-on, there are a number of policy measures that policymakers should considered:

Firstly, instead of being delayed, the implementation of the AfCFTA should be speeded up, with the involvement of all economic operators in the identification of priorities for trade facilitation reforms and enablers for a rapid and ambitious implementation of the agreement. At the sectoral level, fast tracking imports and exports by creating green lanes for medical, pharmaceutical, and food industry are priorities, but also green technologies and green transition products. Trade financing institutions and development banks could play a crucial role in facilitating the financing of the cross-border supply of these products.

The complex consequences of the COVID-19 pandemic, coupled with other crises already impacting Africa (security in the Sahel, draught, locust plague), bring the risks of a mass poverty spiral at a scale the continent has not faced in its recent history.

Secondly, at the continental level, it is then a priority to maintain the momentum towards AfCFTA’s implementation and trade liberalization schemes, as it represents a real trade lever for African countries facing a strong negative impact on their trade with the rest of the world (WTO, 2020). Given the importance of these shocks, combined to the transformative dimension of the Covid-19 with regards to global value chains, African economies could show additional ambitions in attracting and retaining investment first to maintain their firms’ linkages with MNEs in the global production networks and supply chains, but also to promote new investment related to the implementation of the continental agreement. Against this context, many observers call for an ambitious implementation of the AfCFTA and also to resist the temptation to protectionist measures, including the implementation of the African Protocol on Free Movement of Persons, highlighting the necessity to facilitate labor mobility across the continent, including new forms of mobility as digital mobility.

Thirdly, as an increasingly digitized economy is also an accelerator of the emergence of new forms of mobility that are more virtual and could complements local labor and physical mobility, African governments must invest in education and reskilling programs to ensure that technology supplements, instead of replaces labor (Naudé, 2017). Indeed, the fourth industrial revolution is dramatically changing global systems of labor and production, requiring active policies in support of workers and job seekers cultivating the skills and capabilities necessary for adapting rapidly to the needs of African firms and automation more broadly. The AfCFTA can provide the vehicle for going to scale through a pooled African market (Songwe 2020). To achieve this vision, fixing the labor-skills mismatch (Ndung’u 2020) is crucial to make the most of the continental market, particularly when starting Phase II of the AfCFTA negotiations on investment, competition policy, and intellectual property rights. This dimension could be explored in future research inspired by this work.

Suplementary Tables & Figures

Tables and Figures

[1] https://www.imf.org/en/Publications/WEO/Issues/2020/09/30/world-economic-outlook-october-2020

[2]https://www.worldbank.org/en/news/press-release/2020/04/23/most-commodity-prices-to-drop-in-2020-as-coronavirus-depresses-demand-and-disrupts-supply

[3] See https://unctad.org/news/global-foreign-direct-investment-falls-49-first-half-2020

[4] A detailed description of the GTAP data base is provided in Badri Narayanan G. and McDougall (2015)

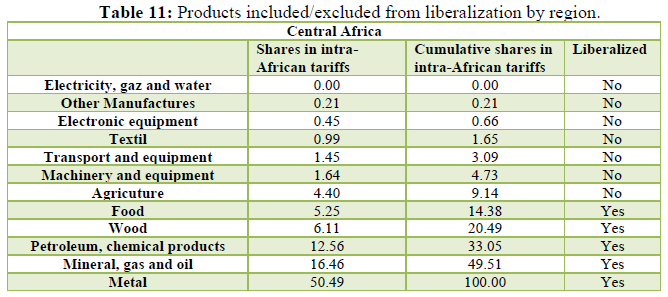

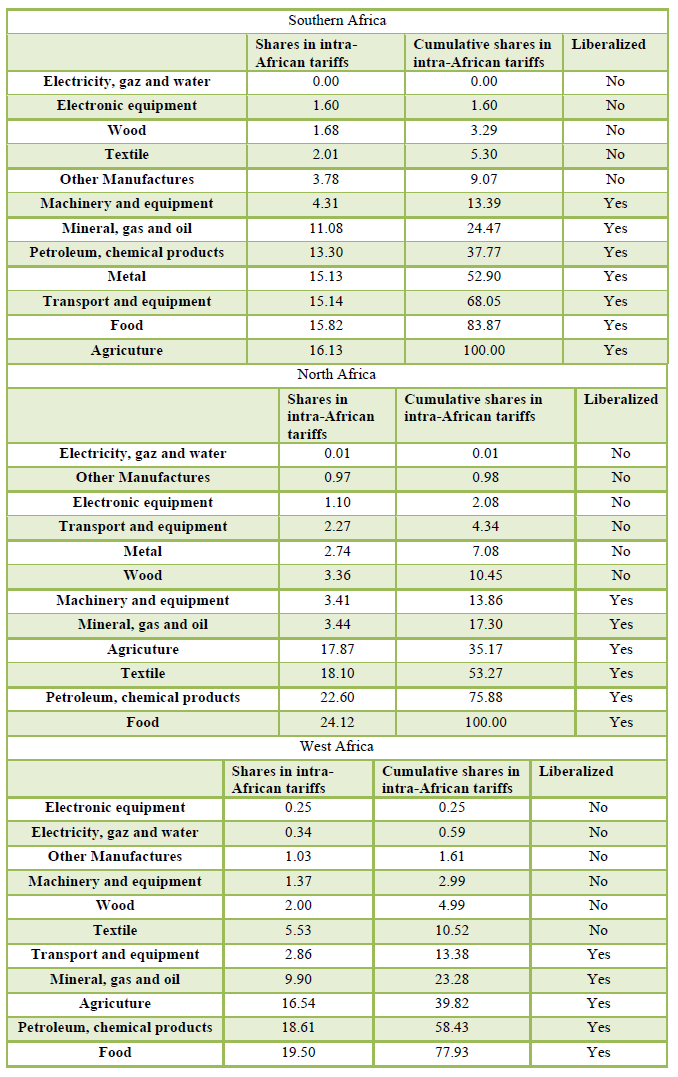

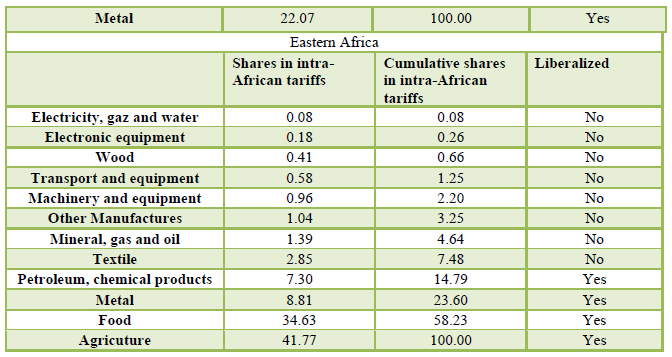

[5] Regarding the products to be included/excluded from liberalization, there are still uncertainties, since the countries are currently negotiating on the issue. In this paper, we have adopted a simple formula for determining which products to exclude from liberalization. First, for each region, the share of intra-African tariffs for each product is computed. Then, the products are classified according to these shares in ascending order. All products with a low share of intra-African tariffs are excluded up to a cumulative share of around 10%. See table 11 in appendices for products included/excludes according to regions

[6] This increase has different dimensions, as presented by the WTO : https://www.wto.org/english/news_e/pres20_e/methodpr855_e.pdf

- Anderson, J.E., & Wincoop, E.V. (2004). Trade Costs. Journal Of Economic Literature 42(3), 691-751.

- Anderson, K., & Martin, W. (2005). Agricultural Trade Reform and The Doha Development Agenda. World Economy 28(9), 1301-1327.

- Badri N.G., & Mcdougall, R.A. (2015). Guide To the GTAP Data Base.

- Baldwin, R., & Eiichi, T. (2020). Thinking Ahead About the Trade Impact Of COVID-19. In Baldwin and Di Mauro. Economics In the Time Of COVID-19 PP: 59-71.

- Benhabib, J., & Jovanovic, B. (2012). Optimal Migration: A World Perspective. International Economic Review 53(2), 321-348.

- Bradford, S., & Lawrence, R.Z. (2004). Has Globalization Gone Far Enough? The Costs of Fragmented Markets, Columbia University Press.

- Caselli, F., Feyrer, J. (2007). The Marginal Product of Capital. The Quarterly Journal of Economics 122(2), 535-568.

- Clemens, M.A., Montenegro, C.E., & Pritchett, L. (2008). The Place Premium: Wage Differences for Identical Workers Across the US Border, The World Bank.

- De La Croix, D., & Docquier, F. (2015). An Incentive Mechanism to Break the Low-Skill Immigration Deadlock. Review Of Economic Dynamics 18(3), 593-618.

- Delogu, M., Docquier, F., & Machado, J. (2018). Globalizing Labor and The World Economy: The Role of Human Capital. Journal Of Economic Growth 23(2), 223-258.

- Fouré, J., Quéré, A.B., & Fontagné, L. (2012). The Great Shift: Macroeconomic Projections for The World Economy at the 2050 Horizon.

- Goldin, I., Knudsen, O., & Mensbrugghe, D. (1993). Trade Liberalization: Global Economic Implications, Organization for Economic Cooperation and Development (OECD).

- Gourinchas, P.O., & Jeanne, O. (2006). The Elusive Gains from International Financial Integration. The Review of Economic Studies 73(3), 715-741.

- Brempong, K.G., & Nyarko, Y. (2015). Education, Internal Remittances and Safety Nets in Africa: Some Evidence. Journal Of African Development 17(1), 1-16.

- Hamilton, B., & Whalley, J. (1984). Efficiency And Distributional Implications of Global Restrictions on Labour Mobility: Calculations and Policy Implications. Journal Of Development Economics 14(1), 61-75.

- Hertel, T.W., & Keeney, R. (2006). What Is at Stake: The Relative Importance of Import Barriers, Export Subsidies, And Domestic Support, In Anderson, K.; Martin, W. (Eds): Agricultural Trade Reform and the Doha Development Agenda. Pp: 37-62.

- ILO (2020). COVID-19 And the World of Work: Impact and Policy Responses. ILO Monitor.

- Iregui, A.M. (2005). Efficiency Gains from The Elimination of Global Restrictions on Labour Mobility, In Borjas, G.J., Crisp, J. (Eds): Poverty, International Migration and Asylum. Springer, Pp: 211-238.

- Kennan, J. (2013). Open Borders. Review Of Economic Dynamics 16(2), L1-L13.

- Klein, P., Ventura, G.J. (2007). TFP Differences and The Aggregate Effects of Labor Mobility in the Long Run. The BE Journal of Macroeconomics 7(1).

- Lamont, O.A., & Thaler, R.H. (2003). Anomalies: The Law of One Price in Financial Markets. Journal Of Economic Perspectives 17(4), 191-202.

- Lemelin, A., Robichaud, V., Decaluwé, B., & Maisonnave, H. (2013). The PEP Standard Multi-Region, Recursive Dynamic World CGE Model Pp: 1-132.

- Mevel, S., Moll De Alba, J., & Oulmane, N. (2016). Optimal Regional Trade-Integration Schemes in North Africa: Toward A Pro-Industrialization Policy. Journal Of Economic Integration 31(3), 569-608.

- Miroudot, S. (2017). The Servicifivstio of Global Value Chains: Evidence and Policy Implications. UNCTAD Multi-Year Expert Meeting on Trade, Services and Development.

- Moses, J.W., & Letnes, B. (2004). The Economic Costs to International Labor Restrictions: Revisiting the Empirical Discussion. World Development 32(10), 1609-1626.

- Moses, J.W., & Letnes, B. (2005). If People Were Money, In Borjas, G. J., Crisp, J. (Eds): Poverty, International Migration and Asylum. London, Palgrave Macmillan UK, Pp. 188-210.

- Naudé, W. (2017). Entrepreneurship, Education and the Fourth Industrial Revolution in Africa. IZA Institute of Labor Economics Discussion Paper 10855.

- Ndug'u Njuguna. (2020). Capturing The Fourth Industrial Revolution: A Regional and National Agenda. In Foresight Africa 2020, Brookings.

- Nyarko, Y. (2011). The Returns to The Brain Drain and Brain Circulation in Sub-Saharan Africa: Some Computations Using Data from Ghana. National Bureau of Economic Research Working Paper Series.

- Nyarko, Y., & Brempong, K.G. (2011). Social Safety Nets: The Role of Education, Remittances and Migration.

- Pritchett, L., Gaddy, C.G., & Johnson, S. (2006). Boom Towns and Ghost Countries: Geography, Agglomeration, And Population Mobility [With Comments and Discussion]. Brookings Trade Forum 1-56.

- Samuelson, P.A. (1948). International Trade and The Equalization of Factor Prices. The Economic Journal 163-184.

- Samuelson, P.A. (1949). International Factor-Price Equalization Once Again. The Economic Journal 59(234), 181-197.

- Songwe, V. (2020). A Continental Strategy for Economic Diversification Through the AfCFTA and Intellectual Property Rights. In Foresight Africa 2020, Brookings.

- Tong, Q. (2010). Wages Structure in The United Arab Emirates, Zayed University, Institute for Social and Economic Research.

- UNECA. (2020). Report On African Ministers of Finance Meeting: Emergency Request to The International Community On COVID-19 Response.

- Van Der Mensbrugghe, D., & Holst, D.R. (2009). Global Economic Prospects for Increasing Developing Country Migration into Developed Countries.

- Walmsley, T.L., & Winters, L.A. (2005). Relaxing The Restrictions on The Temporary Movement of Natural Persons: A Simulation Analysis. Journal Of Economic Integration 20(4), 688-726.

- World Bank. (2001). Global Economic Prospects and The Developing Countries 2002: Making Trade Work for The World's Poor, World Bank Group.

- World Trade Organization. (2020). Methodology For the WTO Trade Forecast of April 8.

- Zidouemba, P.R., & Jallab M.S. (2020). The African Continental Free Trade Area and The Trade Facilitation Agreement: Some Regional Macroeconomic Impacts Forthcoming in International Journal of Trade and Global Markets.

-

Table 1

Table 1 -

Table 2

-

Table 3

-

Table 4

-

Table 5

-

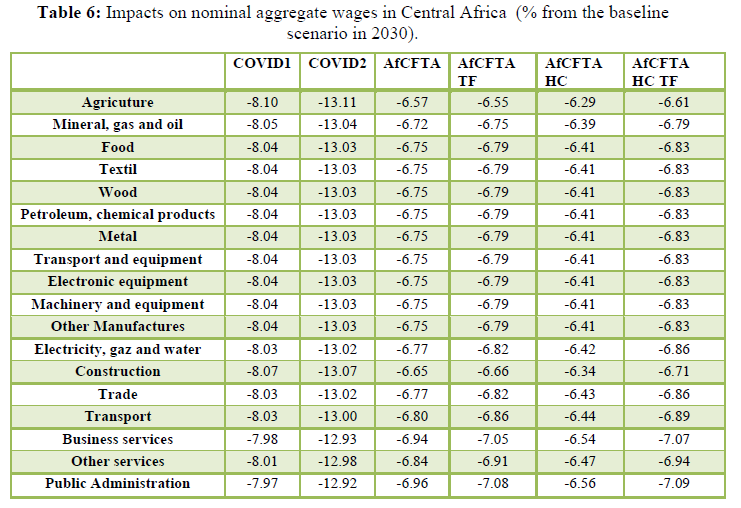

Table 6

-

Table 7

-

Table 8

-

Table 9

-

Table 10

-

Table 11

-

Table 12

-

Table 13