99

Views & Citations10

Likes & Shares

Keywords: Intervention programme, Monetary policies, Inflation, GDP

According to Tule, (Ogundele & Apinran, 2018) the poor performances of monetary policies in Nigeria could be as a result of adopting policy instruments that restrict monetary policy's contributions to economic development. Also, Farmer (2012) posits that the problem with the conventional monetary policy is that, they are best modelled as rules, rather than discretions on events. He continued that since expectation dictates the response of economic agents, monetary policies must change with changing circumstances, hence the need for the increasing implementation of unconventional programs.

Furthermore, the ineffective complements of fiscal policies to monetary policies contributes to the poor outcomes of monetary policies in Nigeria. Historically, efficient human capital and infrastructural development through effective fiscal policies were highly instrumental to the growth in the advanced countries and the growth miracle of the Asian-Tigers (Gaw, 2016). On the contrary, human capital and infrastructural development have suffered years of neglect in Nigeria due to lack of financial resources, poor policy formulation and implementation as well as corruption. These results to inadequate human capital, inadequate infrastructural development and poor business environment in the country (World Bank, 2018). An African Development Bank report on the Nigerian economy shows that insufficient qualitative and quantitative infrastructure is a key development constraint in the country (AfDB, 2010). (Foster & Pushak, 2011). show that addressing Nigeria's infrastructure challenges as at 2011 would require a sustained expenditure of almost $14.2 billion per year over the next decade, which is about 12 per cent of Nigeria's GDP. (Bamidele,2019). cited the country's finance minister, saying that as of 2019, Nigeria needed $100 billion or ₦GN36 trillion annually to address the infrastructural decay in the country.

Sequel to the above and observing this gap, the CBN has been implementing some intervention programmes and projects relating to Agriculture, Human Capital, Infrastructural Development and other growth-enhancing projects to ensure sustainable development in the country. Some of the intervention programmes and projects are: Agriculture Credit Guarantee Scheme (ACGSF), established in 1978; Interest Draw Back (IDP), established in 2003; Microfinance Policy, Regulatory and Supervisory Framework for Nigeria, established in 2005; Agricultural Credit Support Scheme (ACSS), launched in 2006; Entrepreneurship Development Centers (EDCs), established in 2006; NYSC Venture Price Competition Award, established in 2008; ₦200 Billion Commercial Agriculture Credit Scheme (CACS), established in 2009; Real Sector Support Facility (RSSF); SME Credit Guarantee Scheme (SMECGS), established in 2010; SME Re-structuring and Refinancing Fund (SMERRF), established in 2010; Nigeria Incentive-based Risk Sharing System for Agricultural Lending (NIRSAL), established in 2010; ₦300 Billion Power and Aviation Intervention Fund (PAIF), established in 2010; Micro, Small and Medium Enterprises Development Fund (MSMEDF), established in 2013; ₦300 billion Real Sector Support Facility (RSSF), established in 2014; Anchor Borrowers' Programme (ABP), established in 2015 (Centre for Democracy and Development, 2019). Others include Nigeria Electricity Market Stabilization Fund (NEMSF); Nigeria Textile Intervention Fund; Non-oil Export Stimulation Facility; Youth Innovative Entrepreneurship Development Programme (YIEDP); Export Credit Rediscounting and Refinancing Facility and the recent COVID_19 Support Grant of 2020.

Evidence shows that these interventions by the CBN have increased access to finance by the stakeholders, including the entrepreneurs and farmers; improved the productivity of the beneficiaries, helped in diversifying the economy; and improved income generation in the rural areas (Farmer, 2012; CBN, 2016; CBN, 2018; Olanrewaju, Osabohien and Fasakin, 2020). Nevertheless, the Consumer Price Index (CPI) with November 2009 as the base period was 307.5 as at end December 2019, showing that the weighted price level in the country has increased by over 207 per cent within ten years. The year-on-year inflation has been above the target one-digit level and increased to 13.71 per cent in September 2020. The Deposit Money Bank lending rate has been very high, with the spread between 12-months-deposit and lending rate as high as 24.62 per cent in August 2020. Also, the growth of the economy has been sluggish and unsustainable with recessions in-between. Although the contribution of agriculture to GDP moved from 15.5 per cent in 1981 to 25.16 per cent in 2019, that of manufacturing sector dropped from 10.22 per cent to 9.06 per cent within the same period (CBN Statistical Bulletin, 2019).

Given the definition of monetary policy effectiveness by Rasche and Williams (2007) as the ability of monetary policy to maintain price stability and promote economic growth, the above facts suggest that there is need to empirically investigate the effects of the CBN intervention programmes on the effectiveness of the CBN monetary policies. Notwithstanding the importance of such an investigation, there is a lack of empirical literature in the area. The few studies evaluating the impacts of the programmes as earlier cited are all micro-level studies, leaving the macro level and their spillover effect on the effectiveness of the Bank's monetary policies.

This study was conducted to bridge the gap and find out if the CBN intervention programmes have impacted on the effectiveness of monetary policies in the country. The study was conducted in two phases. The first phase involved finding the impact of the CBN intervention programmes on inflation and output, while the second phase evaluated the effect of the implementation of the programmes on the response of the target variables (inflation and output) to changes in monetary policy rate. The target variables were selected following the school of 'New Consensus' on endogenous money as contained in Rasche & Williams, 2007; Arestis & Sawyer, 2006; Meyer, 2001.

EMPIRICAL LITERATURE

With the recognition that the role of central banks transcends beyond price stability mandate to include the promotion of sustainable economic development, central banks have implemented several intervention programs, sometimes, called unconventional policies. Thus, in the last decade, unconventional programs and tools have increasingly become relevant in promoting effective monetary policy across the globe. The unconventional programs, most of which were thought to be temporal, especially after the global financial crisis 2007-2009 have prevailed in most economies (Santor & Suchanek, 2016).

In the global economy, the unconventional measures employed in the last decade are quantitative easing and negative interest rate. Financial times (2014) and International Monetary Fund (2013) refers to quantitative easing and negative interest rates as unconventional programs employed by central banks to inject liquidity into the economy. Despite the high critics around quantitative easing, central banks being the lender of last resort has the ultimate responsibility to use its policy arsenal to contain financial instability (World Bank, 2012; Figeac, 2014).

According to Santor & Suchanek, (2016) the European Central Bank lowered deposit rates to less than zero in June 2014 with three times further cut, to -0.4 per cent in March 2016. Similarly, the central banks of Japan, Sweden, Switzerland and Denmark all recorded negative policy rates. International evidence provides policy-makers with reasonable confidence that quantitative easing remains a valuable unconventional measure and has served its purpose of providing significant monetary and financial easing by lowering interest rates (Santor & Suchanek, 2016, International Monetary Fund, 2013).

In tandem with quantitative easing, asset holding has continued to increase. The Bank of Japan and the European Central Bank (ECB) have continued to expand their respective asset purchase programmes. They do this on the belief that large-scale asset purchases can enhance central bank’s credibility of forward guidance around low future rates and provide further monetary accommodation (Santor & Suchanek, 2016). Buhler (2017) used the event study methodology to show that the communication of unconventional monetary policy programs employed by the Federal Reserve and European Central Bank significantly reduce Bank and sovereign default risk measured by credit default swap spreads. Though they also show that when announcements reveal a negative economic state and outlook, contrary results are obtained. Boneva, Cloyne, Weale & Wieladek, 2018 combined micro econometric data with macroeconomic shocks to ascertain the impact of unconventional monetary policy in the United Kingdom and the results show that in response to £50 billion of Quantitative Easing (QE), firms' inflation expectations increased by 0.22 percentage points. (Luck & Zimmermann,2020). evaluated the employment effects of the Federal Reserve's quantitative easing policies via a bank lending channel. They found that it increased local consumption, employment in the non-tradable goods sector and employment after the third round of QE.

Mouabbi & Sahuc, (2019) analyzed the impact of unconventional monetary policies by the European Central Bank using a dynamic stochastic general equilibrium model. The results show that, without the unconventional monetary policy, both year-on-year inflation and GDP growth would have been smaller by 0.3 per cent and 0.5 per cent, respectively, over the period 2014Q1- 2016Q1. Abhoff, Belke and Osowski, (2020) applied Qual VAR approach to examine the effects of the European Central Bank's unconventional monetary policies (UMP) on inflation expectations in the Euro area, and the study revealed an increase in medium-term real GDP growth triggered by UMP. Houcine, Abdelkader & Lachi, (2020) also investigated the impact of unconventional monetary policies in the United States of America using a vector autoregression (VAR) and found that the effect of credit facilitation programmes aimed at stabilizing financial markets on expected inflation rates was insignificant. Demiralp, Eisenschmidt & Vlassopoulos, (2017) evaluated the macroeconomics effects of central bank's interventions in the economies of the United States of America (USA), Japan and the United Kingdom using ordinary least squares (OLS) method. They found that the use of unconventional monetary policy by the European Central Bank has allowed the economy to achieve its inflation target, which is capable of stimulating economic growth. However, in the USA, the use of the unconventional monetary policy was shown to have triggered an extreme increase in securities prices. This suggests that intervention by the central bank can have both positive and negative effect on the economy.

More central banks of advanced economies compared to emerging economies adopted larger unconventional programs in terms of foreign exchange and domestic short-term liquidity easing measures. This may have been attributed to the emerging economies’ high level of external vulnerabilities coupled with their limited scope for quasi-fiscal activities (IMF, 2013).

In Nigeria, Central Bank of Nigeria (2018) evaluated the performance of the Commercial Agriculture Credit Scheme (CACS) intervention using both qualitative and quantitative methods of analysis. The results show that access to the loan increased the output growth of the beneficiaries in crop production, livestock production and fishery from an average of 9.96 per cent, 12.0 per cent and 13.37 per cent to 26.69 per cent, 65.33 per cent and 42.63 respectively. It has also led to an increase in output growth in food and beverages manufacturing and textile industry from 10.91 per cent and 28.46 per cent to 84.26 per cent and 35.33 per cent respectively. In line with its objective of employment generation, the number of employees grew from 10443 in 2008 to 70070 in 2017. Olanrewaju, Osabohien & Fasakin, 2020 assessed the impact of Anchor Borrowers Program (ABP) on youth rice farmers' productivity (yield/ha) in Kaduna State, using propensity score matching (PSM) approach. The results show that it increased rice yields per hectare by 42.46 per cent.

STYLISED FACTS

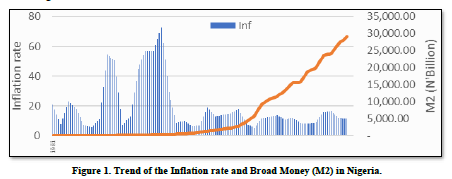

The conventional monetary policies are guided by the already established relationship between and among macroeconomic variables following the macroeconomic theories. However, the existing facts on the relationship between macroeconomic variables sometimes deviate from the established relationship, especially in developing countries. For instance, it has been established that there is a strong positive relationship between broad money supply (M2) and the level of inflation in any economy. On the contrary, existing data for the Nigerian economy, as shown in Figure 1 below shows that the correlation coefficient between inflation and broad money supply in Nigeria between 1981 and 2019 is -0.31.

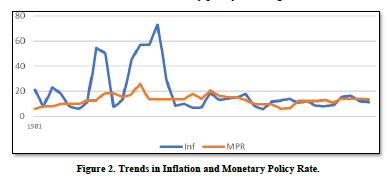

Again, contrary to theoretical expectations, existing data show that between 1981 and 2019, the Monetary Policy Rate (MPR) and inflation in Nigeria has been trending in the same direction, with a positive correlation coefficient of about 0.40. This has two likely implications-that increase in the monetary policy rate in the country increases inflation or that the causal directions are from inflation to monetary policy rate (Figure 2).

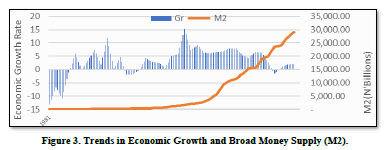

Also, conventional policies expect the M2 to have a strong positive correlation with economic growth following the Mundell-Fleming model. On the contrary, factual data shows that within the review period, there is a very weak correlation with a coefficient of about 0.07 between economic growth and M2 see Figure 3 below A closer look at the figure shows a negative relationship between the variables as from 2002.

METHODS OF ANALYSIS

Analytical Framework

In econometrics literature, the impact of changes in one variable on another variable can be captured in many ways depending on their statistical properties and how they are related. In time series analysis, one important determining factor is the level of integration of the series and whether or not they are cointegrated. This is necessary to avoid spurious results. There is, therefore, need to conduct a unit root and cointegration test before choosing the right model and the method of analysis.

For a mixture of I(0) and I(1) variables as in our case, there is an option of using a Structural Vector Autoregressive (SVAR) model or the Autoregressive Distributed Lag (ARDL) model. The SVAR addresses the limitations of the standard VAR and VEC model by allowing estimations of the structural parameters in the model and the use of a combination of I(0) and I(1) variables without affecting the impulse response and forecasting power of the model. However, the SVAR is used for capturing the impact of innovative shocks and not predetermined and announced interventions, which is the focus of this paper. To this end, we used the ARDL model.

According to Green (2008), "ARDL is a standard least-squares regression that includes lags of both the dependent variable and explanatory variables as regressors". Pesaran and Shin (1998) and Pesaran, Shin and Smith (2001) concludes that the ARDL is the best model for examining the relationship between cointegrating variables especially a mixture of I(0) and I(1) variables. Given as the dependent variable and as explanatory variables, an ARDL () is given as:

where and are the coefficient of the linear trend, the lags of the dependent variable and the k regressors respectively, with as the constant term and the error term. With as the usual lag operator, and the lag polynomial , and , defined as:

and

Equation (1) can be represented as:

Since the study will also analyze the impact of the CBN intervention programmes on the core policy target variables as well as their impact on the effectiveness of monetary policy, the study also employed a segmented model (Gujarati, 2006).

MODEL FORMULATION

As contained in the analytical framework, determining the impact of the CBN intervention programme on the effectiveness of monetary policy was addressed in two stages. The first stage estimated the impact of the intervention programmes on inflation and output growth, which are the ultimate target variables of the monetary policies and the intervention programmes, while the second stage evaluated the impact of the implementation of the programmes on the response of inflation and output to changes in the monetary policy rate.

The first stage used an ARDL model given that there is a mixture of I(1) and I(0) variables in the model. Adopting Equation 1, the model is stated as:

where is the inflation rate and is a vector of explanatory variables including the monetary policy rate (MPR); liquidity ratio (LR)); naira exchange rate (Exr); output growth rate (GR); funds disbursed for the intervention programmes (LDC); gross fixed capital formation (GFCF); crude oil price (Oilp); the volume of remittances (REM); external reserve (RES) and foreign interest rate (Rf).

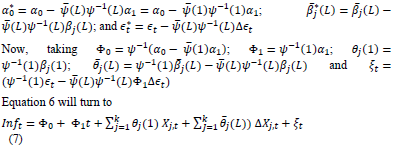

The first stage of the ADRL analysis regresses the dependent variable on its lag and contemporaneous as well as the lagged values of the regressors, through the intertemporal dynamic regression. This was done by decomposing in (3) into using Beveridge-Nelson result giving:

The next stage in the analysis is the derivation of the long-run dynamic relationships between the dependent variable and the regressors by solving for the dependent variable in terms of the explanatory variables as follows:

where

Equation 7 will, therefore, be used to estimate the long-run dynamic relationship between inflation and the regressors, explained in Equation 4. The final stage in ARDL estimation is the computation of Conditional Error Correction (CEC) and the Bounds test, by reducing the vector autoregression framework to its corresponding conditional error correction (CEC) form. Still making use of the Beveridge-Nelson decomposition, the CEC from the ARDL model of Equation 4 is given as:

The Bounds test is a cointegration test, done by testing the significance of the parameters in the CEC model of Equation 8, using an F or Wald test.

The second stage of the study used a segmented model to find out the impact of implementing the intervention programmes on the responsiveness of inflation and output to changes in the monetary policy rate. The period of the analysis (1980Q1-2019Q4) was segmented into three sections - the pre-intervention section (1981-2000), the period of moderate intervention (2001-2010) and the period of massive intervention (2011-2020). We acknowledge that there were few interventions before 2000, but relative to the number and volume of interventions available in the other periods, they are assumed to be negligible. Following the method of model segmentation, two dummy variables were generated for the moderate and massive intervention periods and included in the model are both the multiplicative and additive form as given in Equation 9 below.

is the dependent variable of interest - inflation and output, while is a vector of other variables that affects Y. The variables for the inflation model include the monetary policy rate (MPR); one and two-period lags of inflation; Naira exchange rate (Exr); liquidity ratio (LR) and its one and two-period lags; output growth rate (GR) and its two-periods lag; and gross fixed capital formation (GFCF) and its two-period lag. For the output model, the X vector includes the monetary policy rate (MPR); two-period lags of GDP; exchange rate (Exr) and its one-period lag; crude oil price (Oilp) and its two periods lag; remittances (Rem) and its one-period lag and official development assistance (ODA) and its one-period lag.

Preliminary Data Analysis

To ensure robust and unbiased analysis, series of preliminary tests including tests for structural breaks, stationary and cointegration tests were conducted. The tests revealed the characteristics of the data and informed the modification of the model and the variables used for the analysis. Also, post estimation tests, residual serial correlation LM tests, the residual portmanteau tests for autocorrelations and Ramsey's reset tests were carried out to ensure that the result fulfilled the underlying assumptions of the models.

Data requirement

The analysis employed quarterly time-series data from the fourth quarter of 1981 to the fourth quarter of 2019. The period helped us in capturing the three different stages of intervention used in the segmented model.

RESULTS AND INTERPRETATIONS

Unit root tests

The result in Table 1 contains the unit root test, showing the level of integration of the variables used in the models. The test was conducted using different approaches depending on whether the variable has a structural break or not. This was necessary for, unit root tests without considering structural breaks gives misleading results. In the table, DFBP means that the test was done using augmented Dickey-Fuller test with structural breaks, while DF means that there was no structural break in the variable and the normal Dickey-Fuller unit root test was used. The results show that the order of integration of the variables in the model is mixed, some are stationary at a level while others are integrated of order one.

Post estimation tests

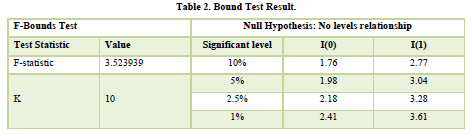

Having ascertained that some of the variables are I(1) and others I(0), the first post estimation test was that of cointegration using the Bounds test. In the conditional error correction (CEC) output, the first lag of inflation is marked with an asterisk, indicating that the p-value is incompatible with the t-Bounds distribution Pesaran, Shin, and Smith (2001). However, the F-statistics is 3.52, which is above the 2.5 per cent upper threshold value of 3.28, showing that the variables are cointegrated (Table 2). The serial correlation test was conducted using the Breusch-Godfrey serial correlation LM test, and the result could not reject the null hypothesis of no serial correlation even at 10 per cent level of significance as the probability was 0.118. Also, Ramsey's RESET test was used to test for model specification error and both the t- and F-statistics could not reject the null hypothesis of correct model specification at 5 per cent level of significance as their probability values were both 0.40.

Impact of the intervention programmes on inflation

The post estimation tests of the ARDL model show that the model is adequate for the analysis. The adjusted R-squared is 0.988, indicating that 98.8 per cent of variations in inflation is accounted for by the variations in the explanatory variables. Also, the F-statistics has a probability of 0.00, indicating that the coefficients of the variables in the model are jointly significant. Although the non-stationarity of some of the variables in the model at level form implies that the model is not dynamically stable in the short run, the coefficient of the error correction term is -0.0745, with a t-value of -6.77. The probability value shows that it is statistically significant even at 1 per cent level and that 7.45 per cent of the short-rum disequilibrium is corrected every quarter towards long-run equilibrium. The result, however, shows that the intervention programmes and monetary policy rate have no significant impact on inflation in Nigeria both in the short and long-run.

Impact of the intervention programmes on Gross Domestic Product (GDP)

Since the goal of CBN includes promoting sustainable economic growth, the study also analyzed the impact of the CBN's interventions on the economy's output using the ARDL estimation method. The post estimation tests of the ARDL model show that the model is adequate for the analysis. The adjusted R-squared is 0.999, indicating that 99.9 per cent of the variations in GDP is accounted for by variations in the explanatory variables. Also, the F-statistics has a probability of 0.00, indicating that the coefficients of the variables in the model are jointly significant. The Bounds test shows that there is cointegration among the variables in the model. The coefficient of the error correction term is -0.0635, with a t-value of -9.44, indicating that it is statistically significantly different from zero and that 6.35 per cent of the short-rum disequilibrium is corrected every quarter towards long-run equilibrium. The coefficient of the intervention programme in the long-run relationship is 0.047, showing that a unit increase in the amount spent on the programmes increases the GDP by 0.047 unit. The result, however, shows that this change is significant at a 7 per cent level and above.

Impact of the intervention programmes on the effectiveness of monetary policy

The study used a segmented model as explained in the method of analysis to address the main objectives of the model by segmenting the period of analysis into three-the preintervention period (1981-2000), the moderate intervention period (2001-2010) and the massive intervention period (2011-2020). An interactive dummy approach was used to analyze the impact of introducing and implementing the intervention programmes at these periods on the responsiveness of inflation and output to changes in the monetary policy rate.

From the segmented inflation model, the coefficients of the interactive dummies for the periods of moderate and massive intervention are -0.13 and -0.0088, with t-values of -1.03 and 0.026, respectively. These show that there was no significant difference between the response of inflation to changes in monetary policy rate within the periods of intervention and the period of no intervention that was analyzed. The result shows that across the periods, inflation was not responding significantly to changes in the monetary policy rate. In other words, the introduction and implementation of the CBN intervention programmes had no significant impact on the effectiveness of monetary policy in controlling inflation in Nigeria.

The segmented output model result shows that the coefficient of the interactive dummy for the period of moderate intervention and the period of massive intervention are -19.84 and 73.69, with t-values of 1.486 and 1.864, respectively. These also show that there was no significant difference between the responsiveness of output to changes in the monetary policy rate within the pre-intervention and intervention periods. However, the coefficients of the additive dummies for the periods of moderate and massive intervention are respectively 35.56 and 91.45, with t-values of 1.46 and 2.44. These show that there is a significant difference between the outputs during the periods of massive intervention and pre-intervention. Specifically, the output during the period of massive intervention is ₦91.45 billion higher than the pre-intervention period, other things being equal.

CONCLUSIONS AND RECOMMENDATIONS

The CBN has been implementing some intervention programmes and projects relating to agriculture, human capital and infrastructural development, youth empowerment programmes and other growth-enhancing projects to supplement the conventional monetary policy and boost its contribution to sustainable development. This study was conducted to find out if the CBN intervention programmes have impacted on the effectiveness of monetary policies in the country. The study was conducted in two phases. The first phase analyzed the impact of the CBN intervention programmes on inflation and output using an ARDL technique since some of the variables in the model are stationary, while others are integrated of order one. The second phase evaluated the impact of the programmes on the responsiveness of inflation and output to changes in the monetary policy rate using a segmented model. The results show that the intervention programmes and the monetary policy rate have no significant impact on inflation in Nigeria both in short and in the long-run. However, in the long run, a unit increase in the amount spent on the programmes increases the GDP by 0.047 unit, which was found to be statistically significant at 7 per cent level.

On the impact of the intervention programmes on the effectiveness of the monetary policy, the segmented inflation model result shows that there is no significant difference between the responsiveness of inflation to changes in monetary policy rate within the periods of pre, moderate and massive interventions. In other words, the introduction and implementation of the CBN intervention programmes had no significant impact on the responsiveness of inflation to changes in the monetary policy rate in Nigeria. Also, the segmented output model results show that there is no significant difference between the responsiveness of output to changes in the monetary policy rate between the intervention and pre-intervention periods. However, the coefficients of the additive dummies show that there is a significant difference between the output during the period of massive intervention and pre-intervention periods. Specifically, the output during the period of massive intervention, other things being equal is ₦91.45 billion higher than that of pre-intervention periods. This confirms the result from the ARDL model that the intervention programmes have a positive impact on output in the long run.

POLICY RECOMMENDATIONS

Although the results from the study show that the implementation of the CBN intervention programmes has not affected the responsiveness of inflation and output to changes in the monetary policy rate, they show that implementation of the programmes has a positive impact on output. More so, the positive impact becomes more significant with increase in the number of programmes and the volume of the intervention fund. We, therefore, recommend that given the new normal occasioned by Covid-19 pandemic and the ineffectiveness of the conventional monetary policies, the Bank should sustain its intervention programmes but there is a need to evaluate the effects of the interventions sector wise to know the right sector to focus on.

- Abhoff, S., Belke, A., & Osowski, T. (2020). Unconventional monetary policy and inflation expectations in the euro area. Ruhr Economic Papers. pp: 837.

- Adesola, I. (2018). Fiscal & Monetary Policies in Nigeria: Key Aspects, Performance, and Policy Options. Journal of Social Science Research 12, 2804-2818.

- AFDB. (2010). An Infrastructural Action Plan for Nigeria Closing the Infrastructural Gap and Accelerating Economic transformation. Available online at: https://www.afdb.org/fileadmin/uploads/afdb

- Akinjare, V., Babajide, A.A., Isibor A. A. & Okafor, T. (2016). Monetary Policy and its Effectiveness on Economic Development in Nigeria. International Journal of Business Management 10, 5336-5342.

- Arestis, P. & Sawyer, M. (2006). The nature and role of monetary policy when money is endogenous. Cambridge Journal of Economics.

- Bamidele, A.A. (2019). Nigeria Needs $100 billion annually to fix infrastructural deficit. Nair metrics. Available online at: https://nairametrics.com/2019/09/24/nigeria-needs-100-billion-annually-to-fix-infrastructural-deficit-finance-minister/

- Boneva, L., Cloyne, J., Weale, M., & Wieladek, T. (2018). The effect of unconventional monetary policy on inflation expectations: Evidence from firms in the United Kingdom. International Journal of Central Banking, 12, 161-195.

- Buhler (2017). The Impact of Unconventional Monetary Policy on Banking and Sovereign Default Risk. Being a Master’s Thesis, University of Amsterdam.

- CBN. (2011). Monetary and Fiscal Policy Coordination: Understanding Monetary Policy Series Central Bank of Nigeria. Available online at: www.cbn.gov.ng

- CBN. (2019). Statistical Bulletin. 30, Abuja.

- Central Bank of Nigeria (2016). Unconventional Monetary Policies. Central Bank of Nigeria Education in Economics Series, 5. Available online at: https://www.cbn.gov.ng/out/2017/rsd/education%20in%20economics%20series%20no.%205.pdf

- Central Bank of Nigeria (2018). Commercial Agriculture Credit Scheme Evaluation and Impact Assessment Report

- Centre for Democracy and Development. (2019). An Assessment of the Effectiveness of Government Policies and Programmes on Economic Growth and Development.

- Demiralp, S., Eisenschmidt, J., & Vlassopoulos, T. (2017). Negative interest rates excess liquidity and bank business models: Banks' reaction to unconventional monetary policy in the euro area. Excess Liquidity and Bank Business Models: Banks' Reaction to Unconventional Monetary Policy in the Euro Area.

- Farmer R. E. A. (2012). The Effect of Conventional and Unconventional Monetary Policy Rules on Inflation Expectations: Theory and Evidence. National Bureau of Economic Research working paper, 18007.

- Figeac, J. (2014). Conventional and unconventional tools of Central Banks. Current challenges. Available online at: https://www.researchgate.net/publication/319519929_Conventional_and_unconventional_tools_of_Central_Banks_1994-2014_Current_challenges

- Financial Times (2014). Europe shows negative interest rates not absurd and might work. Published by Ralph Atkins London Retrieved from internet. Available online at: http://www.ft.com/intl/cms/s/0/db1f5da4-3e89-11e4-a620-00144feabdc0.html#axzz3IUV28Gzc

- Foster, V. & Pushak, N (2011). Nigeria's Infrastructure A Continental Perspective. World Bank Washington DC 20433 USA.

- Gaw, K. (2016). The Story Behind the Four Asian Tigers. Available online at: https://www.idealsvdr.com/blog/the-four-asian-tigers/

- Gujarati, D. N. (2003). Basic Econometrics, McGraw-HiII/lrwin, Fourth Edition. New York, NY, 10020.

- Houcine, B., Abdelkader, A., & Lachi, O. (2020). The Impact of Unconventional Monetary Policy Tools on Inflation Rates in the USA. Asian Economic and Financial Review, 10, 628-643.

- International Monetary Fund (IMF). 2013. Unconventional Monetary Policies-Recent Experience and Prospects

- Ishi K., Stone M. & Yehoue E. B. (2009). Unconventional Central Bank Measures for Emerging Economies. International Monetary Fund working paper, pp: 226. Available online at: https://www.imf.org/external/pubs/ft/wp/2009/wp09226.pdf

- Luck, S., & Zimmermann, T. (2020). E00mployment effects of unconventional monetary policy: Evidence from QE. Journal of Financial Economics, 135, 678-703.

- Meyer, L. H. (2001). Does money matter? Federal Reserve Bank of St. Louis Review, pp: 83.

- Mouabbi, S., & Sahuc, J. G. (2019). Evaluating the macroeconomic effects of the ECB's unconventional monetary policies. Journal of Money, Credit and Banking, 51, 831-858.

- Okoreie, D. I., Manu, AS & Dak-Adzaklo, C. S. (2017). Relative Effectiveness of Fiscal and Monetary Policies in Nigeria. Asian Journal of Social Science Studies, 2,117.

- Olanrewaju, O., Osabohien, R., & Fasakin, J. (2020). The Anchor Borrowers Programme and youth rice farmers in Northern Nigeria. Agricultural Finance Review.

- Pesaran, M. H. & Shin, Y. (1998). An autoregressive distributed-lag modelling approach to cointegration analysis. Econometric Society Monographs, 31, 371-413.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16, 289-326.

- Phillips, P. C. & Ouliaris, S. (1990). Asymptotic properties of residual-based tests for cointegration. Journal of the Econometric Society, 165-193.

- Rasche, H.R. & Williams, M. M. (2007). The Effectiveness of Monetary Policy. Federal Reserve Bank of St. Louis Review, 89, 447-89.

- Santor, E. & Suchanek, L. (2016). A New Era of Central Banking Unconventional Monetary Policies. Bank of Canada Review.

- Tule, M. K., Ogundele O. S. & Appinran, M., O. (2018). Efficacy of Monetary Policy Instruments on Economic Growth Evidence from Nigeria. Asian Economic and Financial Review, pp: 2222-6737.

- World Bank Institute (2012). Lenders of Last Resort and Global Liquidity`` Rethinking the system. Retrieved from Internet. Available online at: http://wbi.worldbank.org/wbi/devoutreach/article/266/lenders-last-resort-andglobal-liquidity-rethinking-system Accessed 8/11/14

-

Table 1

Table 1 -

Table 2